Thinking about passive investing in real estate syndication and hearing “PPM” for the first time can feel intimidating. A Private Placement Memorandum lays out the full picture of a private real estate deal so you can decide with confidence.

This guide explains what a PPM is, how it works in multifamily investing and real estate development, and which pages deserve your closest attention. You will learn the core terms, typical sections, and practical steps for review, using plain English throughout.

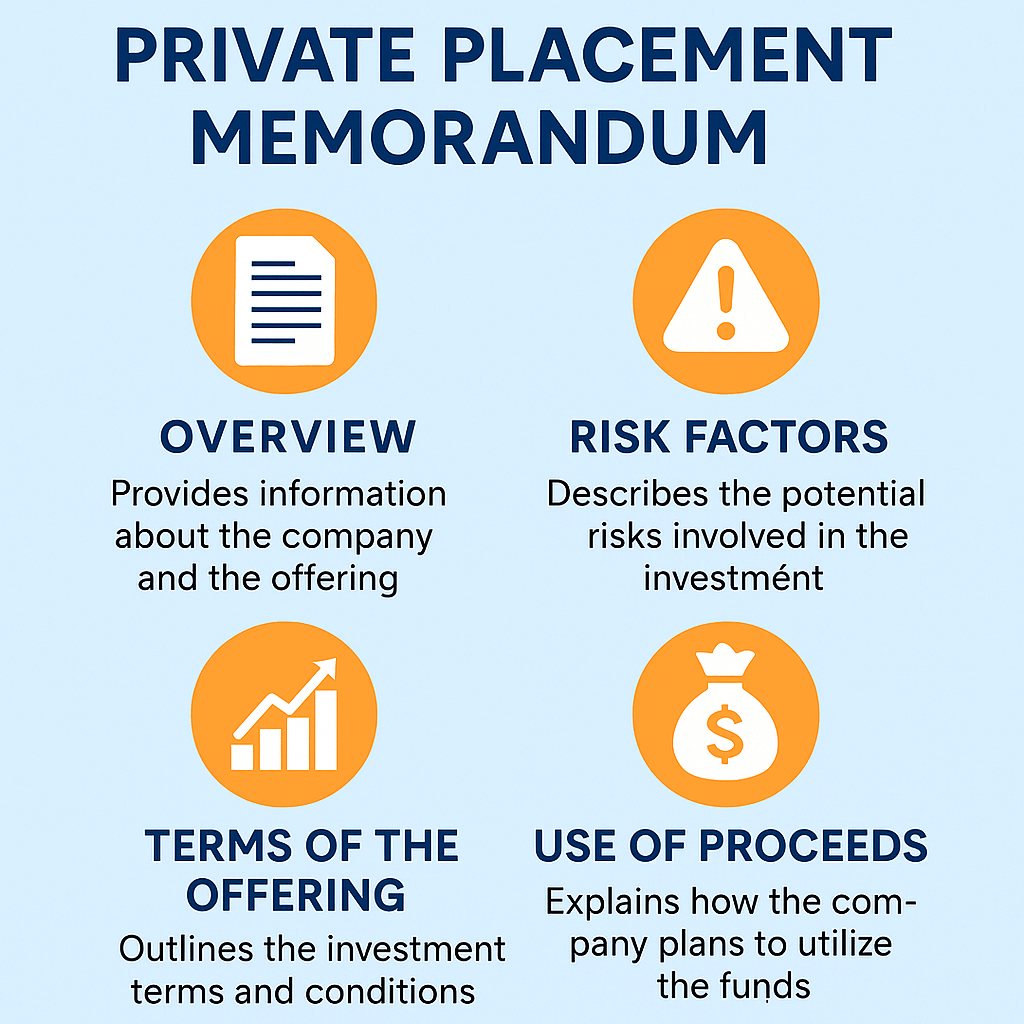

A Private Placement Memorandum is the primary disclosure document for a private securities offering. In real estate syndication, it explains the investment, offers key terms, and discloses material risks so prospective limited partners can make an informed decision. You will also see the term offering memorandum used as a synonym.

Many real estate offerings rely on SEC Regulation D exemptions, especially Rule 506(b) and Rule 506(c). These exemptions let sponsors raise capital without registering the offering, subject to specific conditions such as investor eligibility and required notices.

Every PPM is formatted a little differently, yet most include the sections below. Use this blog as a general roadmap.

Expect clear statements that the securities are not registered, that no public market exists, that transfers are restricted, and that forward-looking statements carry uncertainty. You may also see state “Blue Sky” legends or a NASAA cover legend, which are standardized warnings used by state regulators in private offerings.

A short summary of the real estate asset, strategy, target hold period, and high-level financial goals. This section helps you decide where to dig deeper first.

Look for the exemption being used, often Rule 506(b) or Rule 506(c). Offerings under 506(c) can be generally advertised, but all purchasers must be accredited and the issuer must verify that status. Under 506(b), issuers can accept up to 35 sophisticated but non-accredited investors, and the issuer must have a reasonable belief about accredited status.

A line-item plan for how investor capital will be deployed. In multifamily development or value-add deals, you should see allocations to acquisition, construction or renovation budgets, reserves, fees, and contingencies.

Expect a clear list of fees such as asset management, acquisition, disposition, construction management, and property management. The PPM should state who receives each fee and when fees are paid.

This section explains the preferred return (if any), order of distributions, catch-ups, promotes, and splits between limited partners and the sponsor. It should also describe how profits are handled upon sale or refinance and whether return-of-capital occurs before the promote.

Charts and plain-language descriptions show the GP/LP structure, any co-GPs, and where each class of capital sits in the capital stack. Priority and security for each layer should be clear.

One of the longest sections. Risks usually cover market cycles, interest rates, lease-up timing, construction delays, cost overruns, regulatory changes, environmental issues, financing risks, tax changes, and limited liquidity. Anti-fraud rules require full and fair disclosure of material risks.

Sponsors often manage multiple assets or related companies. The PPM should disclose actual and potential conflicts and how they will be handled.

Look for references to federal securities laws, the Investment Company Act, Investment Advisers Act, “bad actor” disqualification checks, anti-money-laundering rules, and other legal frameworks that apply to private real estate deals.

You will see a high-level summary of partnership taxation, K-1 reporting, basis, allocations, depreciation, and possible consequences on sale or refinance. This section is educational in nature. Always confirm details with your tax advisor.

Instructions cover the subscription agreement, investor questionnaire, funding method, and deadlines. The operating agreement or limited partnership agreement is usually attached or referenced. Read both together with the PPM.

Use this quick checklist during your first pass.

| PPM Section | What to look for |

|---|---|

| Offering Terms | Reg D rule cited, investor eligibility, verification steps, offering size, minimums |

| Use of Proceeds | Hard costs vs soft costs, reserves, contingency, fee line items |

| Fees | Every fee listed, payor and payee, timing and basis calculation |

| Distributions & Waterfall | Preferred return mechanics, order of payments, promote split examples |

| Debt Terms | Leverage, rate type, covenants, IO period, refinance assumptions |

| Risks | Market and deal-specific risks, liquidity and transfer limits |

| Conflicts | Related-party transactions, property management or construction affiliates |

| Reporting | Financial reporting cadence, investor portal access, audit or review language |

Most real estate syndications file a Form D with the SEC within 15 days after the first sale, then make required state notifications. You will not see these filings in the PPM, yet the PPM reflects the same facts disclosed to regulators. Understanding this process explains why the PPM is so detailed.

State “Blue Sky” laws may require notice filings or fees in each investor’s state. Many states accept electronic filings through NASAA’s systems. These rules do not change what you must read in the PPM, but they reinforce the importance of accurate disclosure.

What is the purpose of a PPM in real estate syndication?

It discloses the terms, structure, and risks of a private offering so investors can make an informed decision. PPMs support compliance with securities laws and anti-fraud rules.

Is a PPM legally required for every private deal?

Reg D does not mandate a specific format, but anti-fraud provisions require accurate, complete disclosure. A PPM is the standard way issuers meet those duties.

What is the difference between Rule 506(b) and 506(c)?

506(b) permits a private offering without general solicitation and allows up to 35 sophisticated non-accredited investors. 506(c) allows general solicitation, but all purchasers must be accredited and the issuer must verify that status.

Do I get liquidity in a PPM deal?

Private offerings have limited or no liquidity, and transfers are restricted. Expect explicit transfer restrictions in the PPM.

What filings happen outside the PPM?

Issuers typically file Form D with the SEC and make any required state Blue Sky notices after the first sale.

A Private Placement Memorandum gives you clarity before you invest. By understanding the structure, waterfall, fees, and risk disclosures, you can decide whether a private multifamily investing opportunity fits your goals.

Use the checklist in this article, ask direct questions, and match the PPM against the operating agreement. Clarity leads to better decisions and a smoother passive investing experience.